.webp)

.avif)

Global commerce truly knows no boundaries, with cross-border e-commerce breaking through the $6 trillion ceiling in 2024 - an 8.4% jump from last year. But behind each international sale lies a complex payment journey fraught with potential pitfalls: currency conversions, regional regulations, and unfamiliar payment methods.

These transactions demand specialized expertise that many businesses lack. At Filuet, we've guided companies through these financial labyrinths for over three decades, from managing multi-currency treasuries to streamlining payment processing across continents.

In this guide, we'll walk you through everything you need to know about optimizing your cross-border transactions while minimizing the risks that come with them.

What Makes Cross-Border Transactions Different?

Simply put, a cross-border transaction occurs whenever money moves between entities in different countries. Unlike domestic payments that happen almost instantly, international money movement involves multiple parties, regulations, and systems working together.

These transactions typically fall into several categories:

- B2B (Business-to-Business): These make up the largest volume of cross-border payments, typically involving supply chain payments, service fees, or wholesale purchases between companies in different countries.

- B2C (Business-to-Consumer): When your business sells directly to international customers—think e-commerce platforms like Amazon or Alibaba connecting sellers to global buyers.

- C2B (Consumer-to-Business): Individual customers paying businesses in other countries, such as subscriptions to foreign streaming services.

- C2C (Consumer-to-Consumer): Person-to-person transfers across borders, often for personal payments or marketplace purchases.

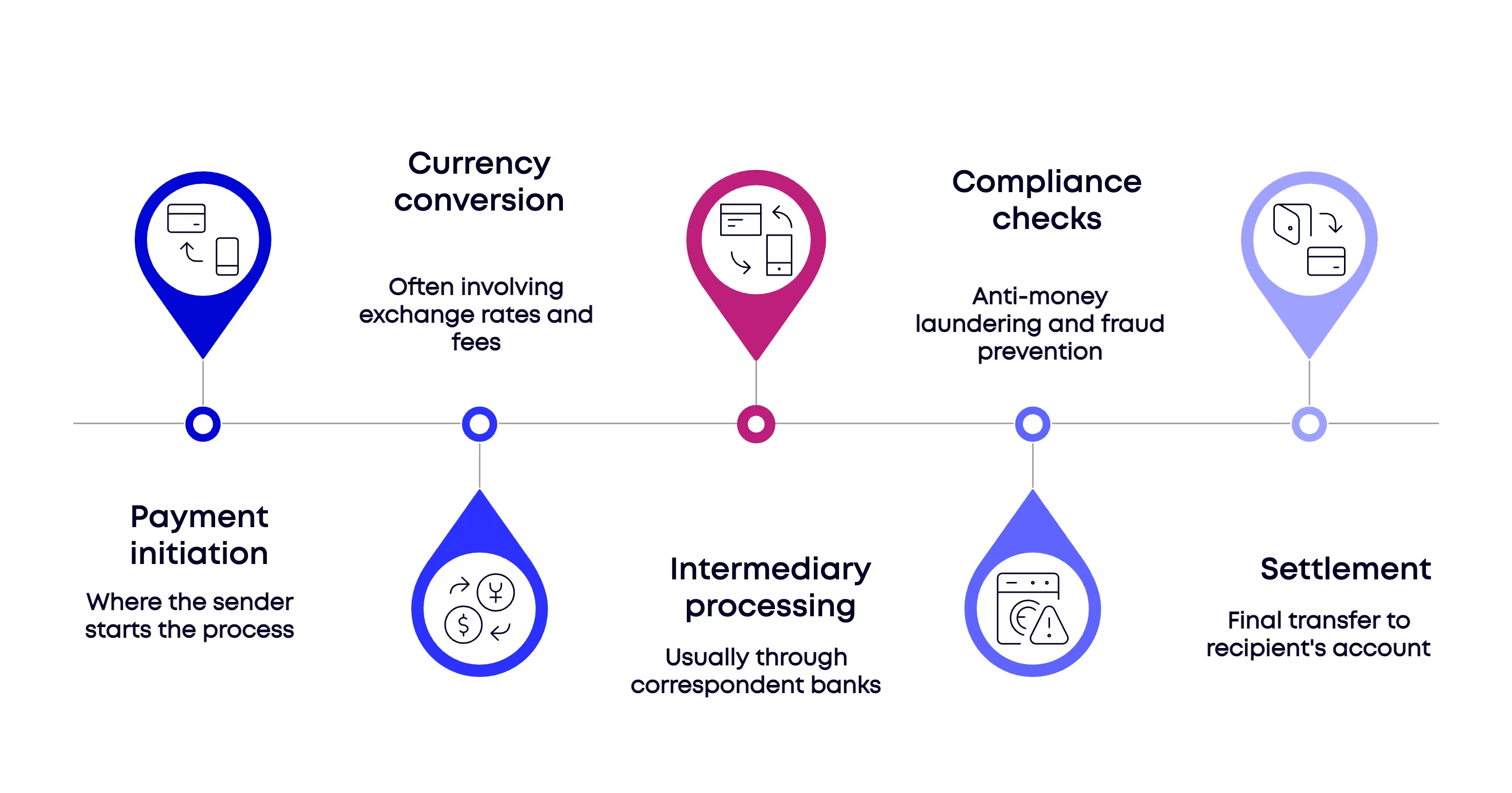

A typical cross-border transaction involves several key components:

This complexity is exactly why many growing companies partner with us for treasury functions that provide centralized control over global financial operations.

Pro Tip: Make sure your treasury management system can handle multiple currencies simultaneously. This capability can save up to 3% in hidden conversion fees that might otherwise eat into your margins.

How cross-border transactions actually work

When you send money internationally, your payment doesn't travel directly to the recipient. Instead, it follows a path through multiple financial institutions.

Most cross-border payments rely on correspondent banking networks. Since banks rarely have direct relationships with every foreign bank, they maintain accounts with partner banks (correspondents) in different countries. Your payment moves between these correspondents until it reaches its destination.

The communication between these banks typically happens through the SWIFT network—a messaging system connecting over 11,000 financial institutions worldwide. But SWIFT doesn't actually move money; it securely transmits payment instructions that tell banks when and where to credit or debit accounts.

Other networks handling cross-border transactions include card networks (Visa, Mastercard), regional systems like SEPA in Europe, and newer digital payment rails offered by fintech companies that aim to make international transfers faster and less expensive.

Convert More Global Customers

Cross-Border Transactions: What You Gain and Risk

Going global opens doors to markets your competitors might miss. With cross-border e-commerce projected to reach $4.81 trillion by 2032 (growing at 18.4% annually), the opportunity is massive.

Companies expanding internationally tap into new customer segments and diversify revenue streams—creating natural hedges against domestic market fluctuations.

Here’s how going global can benefit your business:

- Tap into new customer bases

Expanding internationally allows you to reach untapped markets, increasing your revenue potential. - Diversify revenue streams

Relying on multiple markets helps reduce the impact of domestic market fluctuations. - Leverage counter-cyclical opportunities

Seasonal businesses, like swimwear brands, can maintain year-round cash flow by targeting markets in opposite seasons (e.g., selling to Australia during North America’s winter). - Achieve higher margins

Properly planned global expansion strategy often reveals international markets with better margins than home territories.

However, cross-border success doesn’t come automatically. For instance, transaction costs can eat into profits if not managed properly—FX conversion alone can claim 1–3% of payment value.

Similarly, payment friction can frustrate customers, as lengthy processing times and complex checkout experiences lead to higher cart abandonment rates. Additionally, compliance missteps can result in rejected payments, frozen funds, or regulatory penalties.

Why cross-border payments sometimes fail

"Your payment was declined." Four words no customer or merchant wants to see, yet they appear far too often in cross-border commerce.

Despite technological advances, the "Last Mile" problem—the gap between funds arriving at a destination bank and actually reaching the recipient's account—remains a stubborn issue in cross-border payments.

While Swift reports that 89% of wholesale cross-border payments now reach recipients within an hour (exceeding the G20 target of 75% by 2027), delays still occur due to:

- Local banking hours and settlement windows

- Additional compliance checks at the receiving bank

- Currency controls in certain countries

- Technical integration issues between banking systems

Authorization failures represent another common point of failure. Banks typically decline 5-15% of cross-border transactions—a rate significantly higher than domestic payments. These declines often stem from mismatches between the customer's data and bank records, suspicious activity flags, or simple formatting errors in payment details.

Moreover, chargebacks present yet another cross-border challenge - a staggering 45% of chargebacks filed being fraudulent. These "friendly fraud" cases cost businesses billions annually and are particularly difficult to contest across borders due to documentation and time zone challenges.

Exchange rates and your cross-border business

Currency fluctuations directly impact your bottom line when doing business internationally. Exchange rate movements can affect everything from pricing strategies to profit margins—sometimes dramatically.

The timing of currency conversions can also substantially affect costs. Unfortunately, many businesses suffer unnecessary expenses through several common pitfalls, including:

- Double conversion - Money first converted to an intermediary currency (often USD) and then to the final currency

- Immediate conversion - Converting at transaction time rather than when rates are favorable

- Settlement currency mismatches - Not aligning supplier payments with customer receipts in the same currency

However, smart businesses employ several tactics to manage these risks more effectively:

- Forward contracts lock in exchange rates for future transactions, providing predictability for budgeting and pricing.

- Natural hedging by maintaining foreign currency accounts to receive payments in the same currencies you use to pay suppliers.

- Strategic timing of conversions based on favorable market conditions rather than immediate needs.

Convert More Global Customers

Building Your Cross-Border Transaction Strategy

Creating an effective cross-border payment strategy starts with understanding your specific payment flows. To begin, map out your typical transaction paths—which countries you sell to, payment volumes per corridor, and recurring patterns that could be optimized.

Once you have a clear picture, the next step is to establish multi-currency accounts to reduce unnecessary conversions. These accounts allow you to hold funds in various currencies, giving you the flexibility to pay suppliers or withdraw funds when rates are most favorable.

Additionally, forming strategic partnerships with local payment providers can dramatically improve transaction success rates. These partners bring valuable insights into regional nuances, such as payment preferences, regulatory requirements, and fraud patterns, which global providers might overlook.

.avif)

Recent banking data shows that banks are increasingly partnering with fintech providers to improve their cross-border capabilities—a trend worth watching if you rely heavily on traditional banking channels for international payments.

The art of payment localization

Payment localization is more than just offering multiple payment methods—it’s about creating a trusted, seamless checkout experience for international customers. Here’s how you can optimize your payment process to boost conversions and build trust:

- When it comes to payment methods, local is king

- In China, wallets like Alipay and WeChat Pay handle 81% of e-commerce transactions.

- Dutch shoppers prefer iDEAL for their payments.

- In Brazil, Boleto Bancário is a go-to for online purchases.

- Currency presentation matters just as much

- Showing prices in local currencies eliminates the need for mental exchange rate calculations.

- Customers are 10–25% more likely to spend when they see prices in their native currency.

- Language localization during checkout builds trust

- Beyond basic translations, adapt financial terms, shipping policies, and legal disclosures to fit local contexts.

- A familiar, intuitive checkout experience builds trust and ensures customers feel comfortable completing their purchases.

We've helped numerous B2B and D2C businesses implement localization strategies across diverse markets, and one pattern holds true: the more localized the payment experience, the higher the conversion rates and customer lifetime value.

Cross-Border Payment Methods Around the World

Payment preferences show striking regional variations that businesses must understand to succeed globally. What works in New York often fails in Tokyo or Berlin.

Here is a brief overview:

In Europe, a fascinating shift is underway.

While debit and prepaid cards still lead at point-of-sale in Germany with a 41% market share, digital wallets are rapidly gaining ground. By 2030, they are projected to gain approximately 13 percentage points in market share, which will put them in direct competition with cards.

Meanwhile, North America presents a different picture.

Digital wallets already claim 37% of transaction turnover in 2023, and by 2026, they are forecast to command 41% of e-commerce turnover, surpassing traditional card payments.

On the other hand, the Asia-Pacific region shows the most dramatic digital transformation.

Here, wallets account for 73% of e-commerce payments compared to just 15% for cards. Moreover, in China specifically, digital wallets represent 81% of online transactions, while in the Philippines, they constitute 56% of point-of-sale payments.

Finally, Middle Eastern markets present a unique mix.

While card payments dominate online transactions, accounting for 91% of purchases, cash-on-delivery remains popular and is preferred by 62% of MENA online shoppers. However, digital wallets are making steady inroads, now representing approximately 20% of total online spending in the region.

Smart Ways to Save on Cross-Border Payments

Cross-border payments involve a complex fee structure that can significantly impact your bottom line if not managed carefully. Understanding these costs is the first step toward reducing them.

.avif)

.avif)

The disparity in costs between different payment corridors can also be substantial. For example, sending €5,000 from Western Balkans to EU countries costs approximately 0.50% (€25), compared to just 0.05% (€2.50) for transfers within the EU—a tenfold difference.

To reduce these unnecessary charges, consider these strategies:

- Consolidate payment volumes with fewer providers to qualify for volume discounts

- Negotiate better rates based on your transaction history and projected volumes

- Minimize currency conversions by maintaining multi-currency accounts

- Optimize payment routing by choosing providers with strong local relationships in your key markets

- Time currency conversions strategically rather than converting immediately

Cross-Border Payment Compliance Basics

Dealing with regulatory requirements is, without a doubt, one of the most challenging aspects of cross-border transactions. Over the years, regulations around international payments have become increasingly complicated, growing at an annual rate of 15% over the past decade.

For instance, anti-money laundering (AML) regulations form a cornerstone of the compliance framework. Financial institutions, therefore, must implement strong systems to identify and verify customer identities, assess transaction risks, monitor activities for suspicious behavior, and ultimately report suspicious activities to relevant authorities.

Some of the key AML requirements include:

- Transaction screening against global sanctions and watchlists

- Enhanced due diligence for high-risk transactions

- Continuous monitoring of transaction patterns

- Suspicious Activity Reporting (SAR) to relevant authorities

Additionally, Know Your Customer (KYC) processes serve as the first line of defense against fraud and money laundering.

To comply, financial institutions must verify the identities of both the sender and the recipient before processing international transactions. This typically involves collecting government-issued IDs, proof of address, and, in certain cases, biometric data.

Managing VAT/GST and sales tax internationally

Tax obligations represent one of the most complex aspects of cross-border commerce. Each country, however, applies its own rules for when, how, and at what rate taxes should be collected on international transactions.

In general, the basic principle for VAT/GST collection is that tax should be applied in the jurisdiction where consumption occurs. For physical goods, this typically means the destination country. On the other hand, for digital services, determining the place of consumption becomes more challenging. Most jurisdictions, therefore, use customer location as the determining factor.

Common tax calculation pitfalls include:

- Misidentifying the place of supply: Different rules apply to physical goods, digital services, and other offerings

- Missing registration thresholds: Many countries require registration once sales exceed specific amounts

- Incorrect classification: Products may fall into different tax categories in different countries

- Currency conversion errors: Exchange rate fluctuations can affect tax calculations

- Incomplete documentation: Failing to maintain proper evidence of customer location and transaction details

Keeping thorough records is key to staying compliant. These records should include invoices, contracts, proof of customer location, and evidence of tax collection and remittance. Moreover, many tax authorities now require these records to be maintained for 5-10 years and be readily available in electronic format.

Wrapping Up

Cross-border payments aren't the most glamorous part of running a global business, but they might be the most crucial.

- Every dollar saved on transaction fees goes straight to your bottom line.

- Every friction point removed from your checkout process keeps customers from abandoning their carts.

- Every compliance step properly implemented prevents potential headaches down the road.

The businesses winning the global commerce game aren't necessarily the biggest—they're the ones that have mastered these payment fundamentals. They've done the hard work of localizing their payment stacks, negotiating better FX terms, and building systems that scale across borders without scaling their overhead costs.

We've walked this path alongside hundreds of companies at Filuet, and we've seen firsthand how payment optimization transforms international performance. The strategies outlined here aren't theoretical—they're battle-tested approaches that work in real markets with real customers.

Whether you're dipping your toes into new markets or already operating across continents, there's always room to sharpen your approach.

The question isn't whether you can afford to optimize your cross-border payments—it's whether you can afford not to.